Abstract According to the National Renewable Energy Center, the cumulative installed capacity of photovoltaic power generation in the country has reached 101 million kilowatts, breaking the 100 million kilowatt mark for the first time. For the photovoltaic industry, 2017 is undoubtedly a crucial year, from the abandoned light limit, subsidies drag...

According to the National Renewable Energy Center, the cumulative installed capacity of photovoltaic power generation in the country has reached 101 million kilowatts, breaking the 100 million kilowatt mark for the first time. For the photovoltaic industry, 2017 is undoubtedly a crucial year. From the impact of light and power cuts, subsidy arrears, electricity price cuts, technological progress, etc., the industry has reached a critical crossroads. After years of rapid development, photovoltaics have become an integral part of China's energy system. In the middle of 2017, we have integrated the statistics of the photovoltaic industry of the official and authoritative private organizations, and sorted out the development of the Chinese PV industry in the first half of 2017, hoping to provide a reference for the industry.

According to the National Renewable Energy Center, the cumulative installed capacity of photovoltaic power generation in the country has reached 101 million kilowatts, breaking the 100 million kilowatt mark for the first time. For the photovoltaic industry, 2017 is undoubtedly a crucial year. From the impact of light and power cuts, subsidy arrears, electricity price cuts, technological progress, etc., the industry has reached a critical crossroads.

In this report, we reviewed the PV modules and operations in the first half of 2017 and looked forward to the possible developments in the second half of the year.

Review in the first half of 2017 1. Component links Domestic market: 630 policy has a huge impact. Due to the existence of the 630 policy, the photovoltaic component industry in 2017 is largely repeating the story of 2016. From the data point of view, in the first quarter, due to the low temperature in the three northern regions of China, the construction is inconvenient, the shipment of PV modules has been not prosperous, the price is also slightly depressed, and the profitability of most companies is generally poor; With the 630 limit approaching, market demand has soared and prices have begun to pick up. Corporate profitability has improved.

Overseas markets: Two significant changes are worth noting. First, in general, whether it is silicon wafers, battery chips or components, the export volume of Chinese enterprises has maintained rapid growth, but its export value has decreased significantly year-on-year. This indicates that the export of photovoltaic modules is in the form of price subsidies. The average export price is much lower than last year. Second, from a partial perspective, the international market structure has undergone significant changes. The export volume of mature markets including the United States, Germany, and Japan has declined significantly, while emerging markets including India, Brazil, and Mexico have exploded. increase. This is mainly because Chinese companies have already invested in factories in mature market countries, and shipments are no longer subject to customs statistics.

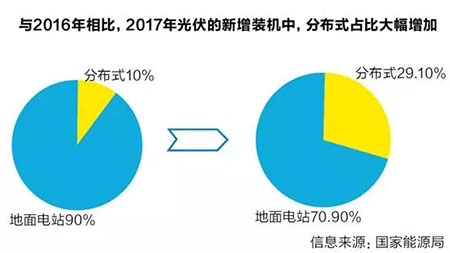

2. Overview of the operation segment market: Distributed PV shows explosive growth. In the operation of photovoltaic power plants, compared with previous years, one of the most obvious features of 2017 is the explosive growth of the proportion of distributed photovoltaic installations. The data shows that in the first half of 2016, the proportion of new PV installations in the country was about 10%, while in 2017 it was 30%, and the installed capacity surged 290%. The reason for this phenomenon is that with the changes in the industry environment, several major advantages of distributed PV are gradually being highlighted. Specifically, there are three main items: First, it is not controlled by national indicators, and only needs to be filed. . If the centralized power station exceeds the scale of the national construction index, the province needs to solve the subsidy funds by itself. Second, the impact on the power grid is small, the possibility of being absorbed is greater, and there is no need to face the power-limiting dilemma. Third, according to the policy, the settlement period of distributed PV subsidies cannot exceed two months, which guarantees the cash flow of the project. Driven by these positives, more and more social capital has begun to focus on distributed power plants, especially household photovoltaics.

Electricity price: The effect of the green certificate replacement subsidy is lower than expected. In the past year, there has been no substantial change in the subsidies for renewable energy. This has led to a more serious situation of subsidy arrears, which has directly led to a redemption crisis for companies such as Lunengbao and other major PV financing businesses. Although the National Energy Administration hopes to replace the new energy subsidies with green certificates, the actual situation is not satisfactory. The data shows that since the green certificate was officially purchased on July 1, 2017, the sales revenue of green certificates has been less than 2 million yuan in half a month, and the current funding gap for renewable energy subsidies is as high as tens of billions of yuan. Far from meeting the real needs.

Overseas markets: Trade barrier risks still need to be guarded. From a fundamental point of view, the photovoltaic industry has great potential for development in the international market. The approval of the Paris Agreement has laid a solid foundation for the development of the global PV market, and the global energy demand has also emerged from a centralized state. Emerging markets have also begun to develop in a large scale. However, due to a series of factors, in 2017 In the past six months, many European, American and Japanese PV module companies have closed down due to poor management. Due to the consideration of the interests of domestic PV module companies, the governments of the above regions and countries have initiated relevant protection procedures to prevent including China. The PV module companies within the country entered the country's market. Some commentators believe that the scope and intensity of this PV trade war is more serious than that in 2012. In the case of limited market growth potential in the second half of the year, the international market is changing, which is undoubtedly a major factor for China's PV module companies. The challenge.

Production costs: Performance growth will help component costs continue to decline. In the first half of 2016, we mentioned that at this stage, the cost reduction of PV modules mainly comes from the following points: First, economies of scale, second, technological development, third, accumulation of management experience, and fourth Optimization of production capacity layout. In this, both the first point and the second point require the support of good performance, thus providing the company with sufficient market capacity and research and development funds. Although there are some uncertainties, on the whole, the decline in the production cost of photovoltaic modules is unstoppable, just a matter of speed.

2) The industry standard for distributed PV in the operation chain will be more perfect. The rapid development of distributed photovoltaics has brought some turnarounds to photovoltaic enterprises that were once in trouble. However, due to the rapid development, distributed photovoltaics have also appeared to be subject to some norms. For example, some products have major problems in quality, design and installation are not standardized and reasonable, and follow-up warranty services can not keep up. We believe that the relevant departments will have a greater chance of issuing standardized policies for distributed photovoltaics, and relevant industry organizations will also The development of corresponding industry standards will lead to a round of reshuffle in the distributed photovoltaic industry. At that time, a group of enterprises with insufficient standards in the industrial chain may be cleaned out.

Renewable energy surcharges are unlikely to increase. At present, reducing costs for entities has become one of the hard requirements of the central government. Under such circumstances, if you want to balance the increase in renewable energy surcharges with the reduction in terminal tariffs, there is only one possibility, that is, to cut other funds in the electricity price and raise the renewable energy surcharge. In this case, both can be considered, and the pressure on public opinion is minimal. However, from the recently released documents, we can see that although the government has cancelled the urban public utilities in the electricity price and compressed the large and medium-sized water conservancy construction fund, the renewable energy surcharge has not been raised at the same time. Under such circumstances, if the relevant departments still want to increase the renewable energy surcharge, there is no doubt that they will face greater pressure. The price of coal-fired benchmarks has also recently risen. From this point of view, the best time to increase the renewable energy surcharge has been missed, and it is unlikely that there will be changes in the second half of the year.

The green certificate system needs to be adjusted. For renewable energy power plants, including photovoltaics, green certificates are by far the most mature and most feasible system. However, the current policy is not conducive to the promotion of green certificates: First, for users who are interested in purchasing green certificates, the current green certificate purchase process is relatively cumbersome, buyers need to log in to the platform, and at the same time register, the operation process is not simple enough. Secondly, for potential users of green certificates, the current policy does not mandate to subscribe for a green card, so for them, buying green power is not a necessity. However, given that the current subsidy gap for renewable energy is expanding, it is necessary to adjust the green certificate policy so that it can afford to fill the subsidy gap. The specific entry points are mainly from two aspects. The first is to simplify the purchase process of green certificates. The second is to promote mandatory (or semi-mandatory) purchase quotas.

Led Iron Panel Light,Led Round Iron Ceiling Light,Led Ceiling Light Round,Led Adjustable Panel Light

Foshan Extrlux Co., Ltd. , https://www.extrlux.com